Introduction

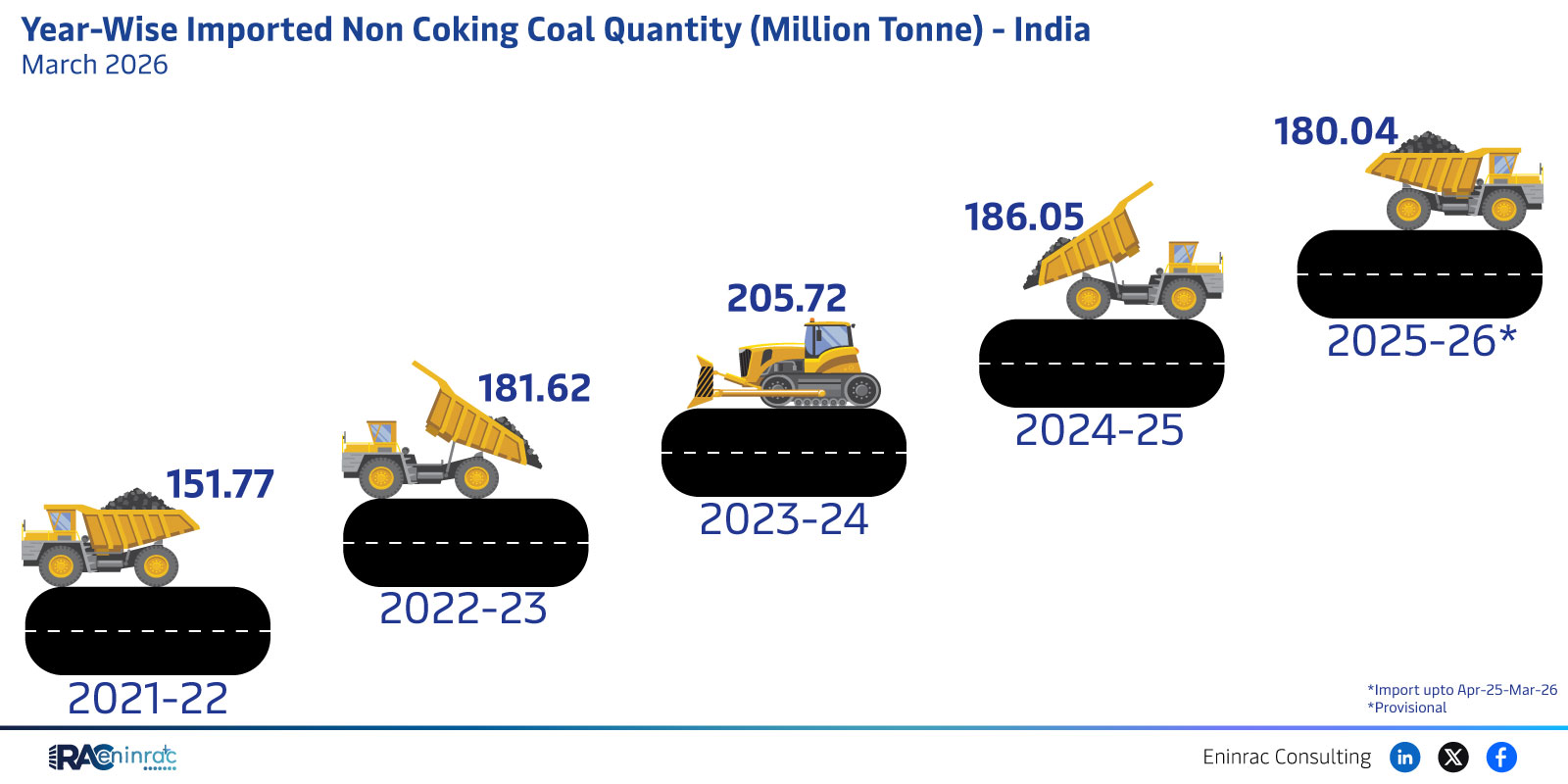

India’s reliance on imported non‑coking coal continues to shape its energy landscape. The latest figures for the fiscal year 2023‑24 show a total import volume of 151.77 million tonnes, highlighting the scale of demand from power generators, steel producers and other heavy‑industry users. This article breaks down what the data means, why it matters for policymakers and investors, and how the trend compares with previous years.

What Does the Data Reveal About This Topic?

The key insight is that India imported 151.77 Mt of non‑coking coal in 2023‑24, a volume that underscores the country’s ongoing dependence on foreign supplies to meet its industrial energy needs. The figure reflects both domestic production shortfalls and the strategic importance of securing reliable coal imports for continuous operations.

Comparative Analysis of Recent Import Trends

When placed alongside earlier fiscal years, the 151.77 Mt figure signals a modest increase from the 2022‑23 period, which recorded slightly lower volumes. The upward movement can be linked to higher steel output, expanded power generation capacity, and tighter domestic coal supply constraints. Regions such as the eastern ports of Paradip and Haldia remain the primary entry points, while major importers include Australia, Indonesia and South Africa. The data also suggests that while overall coal consumption is being scrutinised for environmental impact, non‑coking coal remains essential for specific industrial processes.

Impact on Sectors and Industries

Non‑coking coal imports directly affect the steel sector, where the fuel is used in blast furnaces, and the power sector, which relies on coal‑fired plants for baseload generation. Investors watch these import volumes to gauge demand stability, while policymakers balance energy security with climate commitments. Logistics providers benefit from increased port activity, and domestic coal miners face competitive pressure, prompting calls for efficiency improvements and diversification.

Key Takeaways

- India imported 151.77 Mt of non‑coking coal in FY 2023‑24.

- The volume marks a slight rise from the previous fiscal year, reflecting higher industrial demand.

- Eastern Indian ports continue to dominate as primary entry points for coal shipments.

- Australia, Indonesia and South Africa remain the top supplying nations.

- Non‑coking coal is critical for steel production and baseload power generation.

- Import trends influence investment decisions, policy formulation and domestic mining strategies.

FAQs

Why does India import non‑coking coal instead of using domestic supplies?

Domestic production often falls short of industrial demand, and imported coal offers consistent quality and volume to support steel and power plants.

Which countries are the main exporters of non‑coking coal to India?

Australia, Indonesia and South Africa are the leading suppliers, together accounting for the majority of imports.

How do import volumes affect India’s energy security?

Higher import volumes ensure a steady fuel supply for critical industries, reducing the risk of production interruptions caused by domestic shortages.

What environmental concerns are associated with increased coal imports?

Importing more coal can raise carbon emissions and air‑quality issues, prompting calls for cleaner energy transitions and stricter regulatory oversight.

Will the trend of rising non‑coking coal imports continue?

Future volumes will depend on industrial growth, domestic mining capacity, policy shifts toward renewable energy, and global coal market dynamics.