Introduction

The April 2026 sub‑station capacity development report provides a detailed snapshot of installed megawatt (MW) capacity across major voltage levels and key players in India. Understanding this data is essential for investors, policymakers, and industry analysts who track the growth of the power transmission network and its impact on overall energy security.

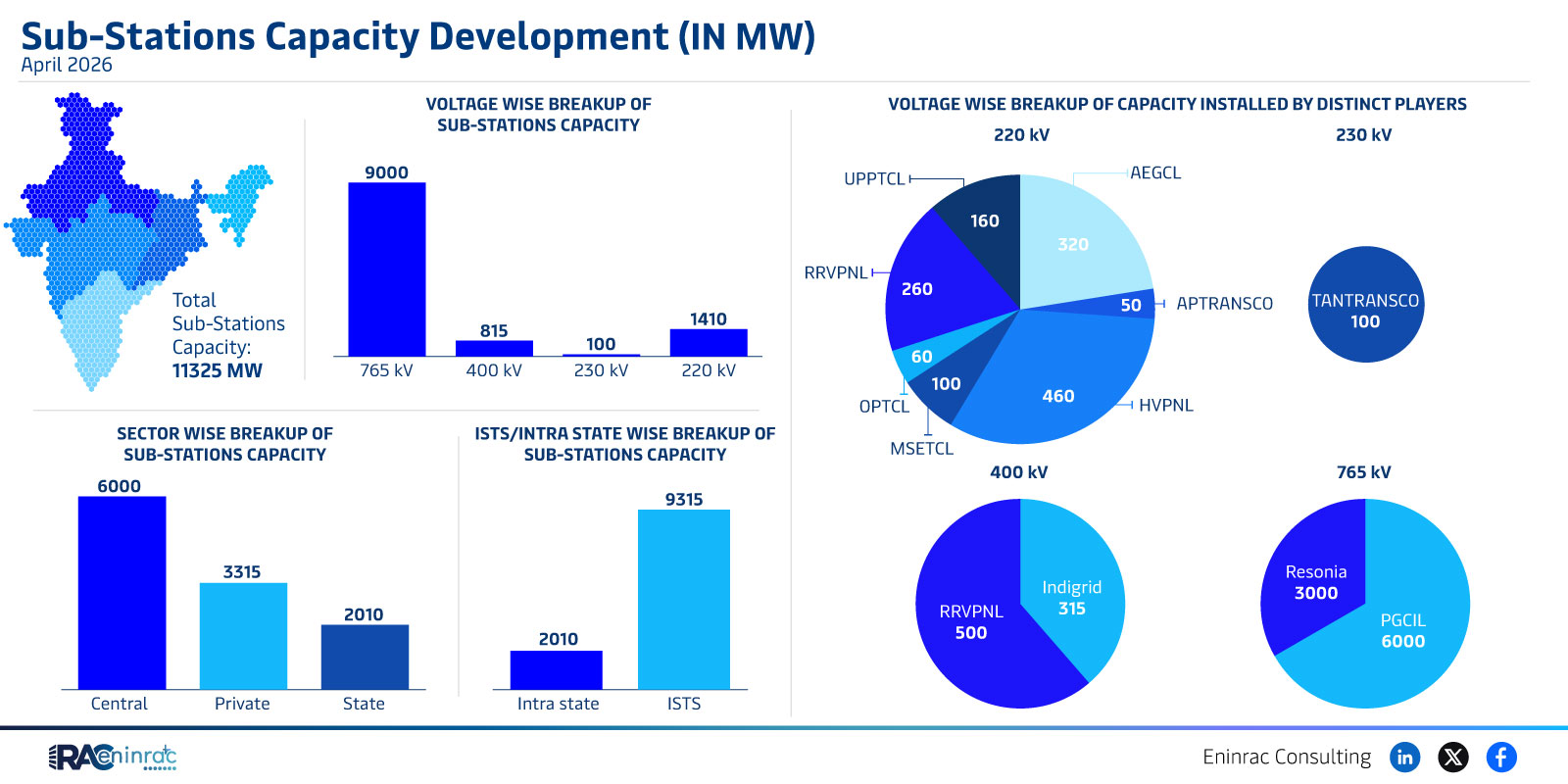

What Does the Data Reveal About This Topic?

Which entities are leading the expansion of 220 kV and 230 kV sub‑stations, and how does the total installed capacity compare across sectors? The figures show that AEGCL, APTRANSCO, and TANTRANSCO together account for a combined capacity of 5,225 MW, with a notable concentration at the 220 kV level (3,815 MW) versus 230 kV (1,410 MW). Additional capacity of 100 MW is listed under a separate category, highlighting smaller but strategic installations.

Voltage‑Level Distribution and Player Contributions

A comparative look at the voltage‑wise breakup indicates that the 220 kV tier dominates the network expansion, driven primarily by AEGCL’s large portfolio. APTRANSCO and TANTRANSCO contribute significantly to the 230 kV segment, suggesting a balanced approach to medium‑voltage reinforcement. The presence of HVPNL and other private sector participants, though modest in absolute numbers, points to growing diversification in grid development.

Impact on Sectors and Industries

Enhanced sub‑station capacity directly influences several critical sectors. For the conventional energy industry, increased transmission capability enables smoother integration of thermal and hydro plants, reducing bottlenecks. Renewable energy projects benefit from improved grid access, while investors gain confidence from the clear expansion roadmap. Policymakers can align infrastructure spending with regional demand forecasts, and utilities can plan maintenance and upgrades more effectively.

Key Takeaways

- AEGCL leads the 220 kV capacity expansion with 3,815 MW.

- APTRANSCO and TANTRANSCO together provide the majority of 230 kV capacity.

- Total reported capacity reaches 5,225 MW across the two primary voltage levels.

- Private players such as HVPNL contribute smaller but strategic capacity additions.

- The data underscores a balanced growth strategy between 220 kV and 230 kV networks.

- Improved transmission capacity supports both conventional and renewable energy integration.

FAQs

Which company has the highest 220 kV capacity?

AEGCL holds the largest 220 kV capacity at 3,815 MW.

How much total capacity is reported for 230 kV sub‑stations?

The combined 230 kV capacity reported for APTRANSCO and TANTRANSCO is 1,410 MW.

What role do private players play in the April 2026 data?

Private entities like HVPNL add modest capacity, indicating emerging participation in grid development.

Why is voltage‑wise capacity important for investors?

It reveals where infrastructure investment is concentrated, helping investors target growth opportunities.

How does increased sub‑station capacity affect renewable energy projects?

Better transmission infrastructure reduces curtailment risk and enables smoother integration of renewable generation.