Introduction

India’s cement output is a key indicator of construction activity and economic health. Recent figures released for fiscal years 2024, 2025 and early 2026 show a subtle shift in production volumes. This article examines the numbers, explains why they matter, and outlines the implications for investors, policymakers and industry players.

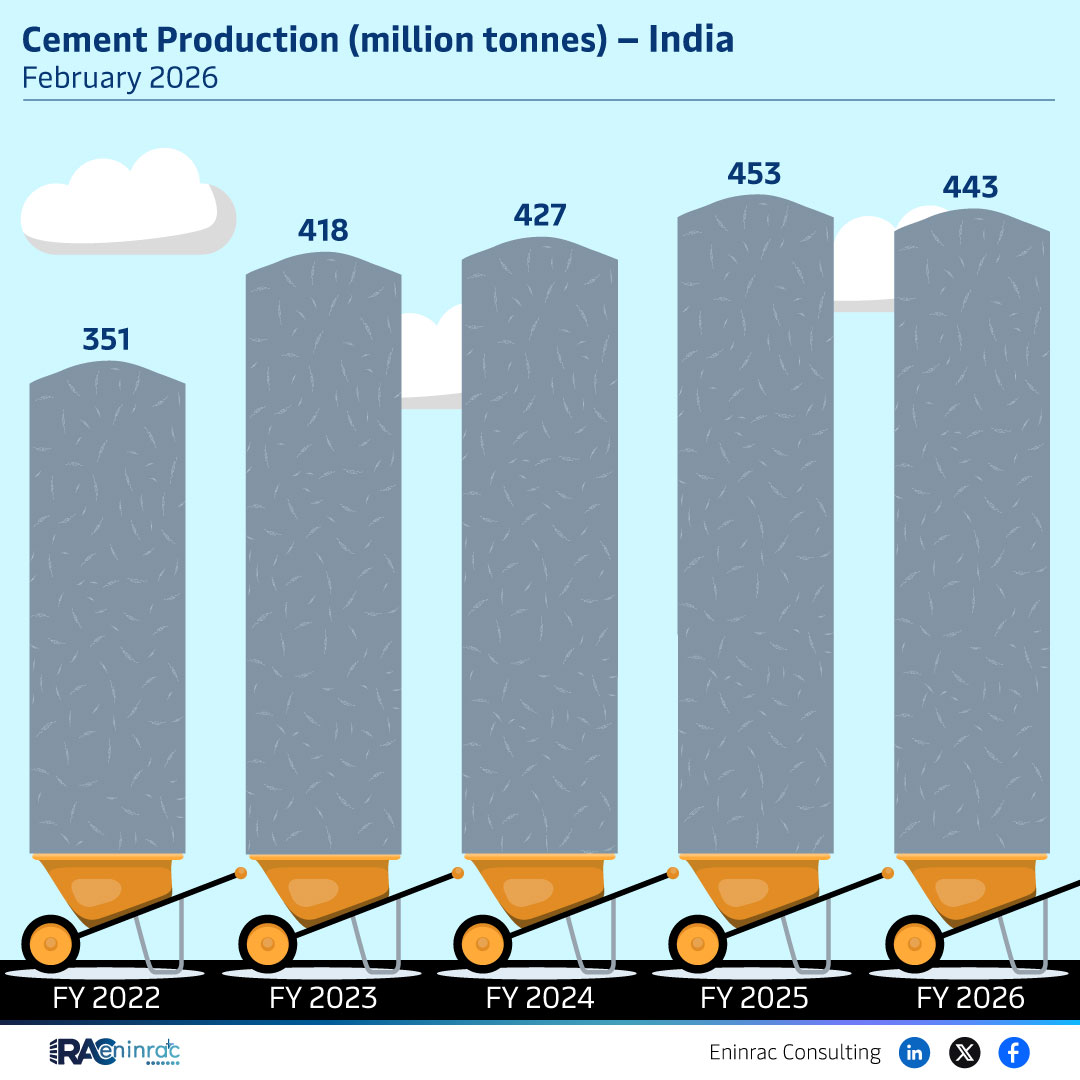

What Does the Data Reveal About This Topic?

The raw data indicates that cement production fell from 453 million tonnes in FY2024 to 443 million tonnes in FY2025, with the latest February 2026 snapshot suggesting a continuation of the downward trend. The question is: what factors are driving this decline and how significant is it for the broader market?

Analyzing the Decline in Indian Cement Output

A comparative look at the three fiscal periods highlights a 2.2% reduction between FY2024 and FY2025. Early 2026 data points to a further dip, reinforcing a pattern of modest contraction. Contributing elements include higher input costs, tighter credit conditions, and a slowdown in residential and infrastructure projects. Regional disparities are evident, with northern states experiencing sharper drops than the southern belt, which remains relatively resilient due to ongoing urbanization projects.

Impact on Sectors and Industries

The downward shift in cement production reverberates across several sectors. Construction firms may face material shortages or higher prices, prompting a reassessment of project timelines. Steel manufacturers, which rely on cement for structural components, could see demand fluctuations. Financial institutions monitoring loan portfolios tied to real‑estate development must adjust risk models. For investors, the trend signals a need to scrutinize company earnings, cost‑management strategies and diversification into alternative building materials.

Key Takeaways

- Cement production fell from 453 Mt in FY2024 to 443 Mt in FY2025.

- Early 2026 data suggests the decline is persisting.

- Higher raw material costs and tighter financing are primary drivers.

- Regional performance varies, with the north showing larger drops.

- Construction and steel sectors may experience cost pressures.

- Investors should monitor company margins and diversification plans.

FAQs

Why did India’s cement production decline in FY2025?

Rising input costs, reduced credit availability and a slowdown in major construction projects combined to lower output.

Is the decline expected to continue in FY2026?

Early 2026 figures indicate a continuation, but the pace will depend on policy measures and market demand.

Which regions in India are most affected?

Northern states have seen sharper reductions, while the southern region remains comparatively stable.

How does this trend affect steel manufacturers?

Reduced cement output can lead to higher cement prices, increasing overall material costs for steel‑related construction.

What should investors watch for?

Focus on cement companies’ cost‑control initiatives, diversification into green building materials and exposure to regional markets.