Introduction

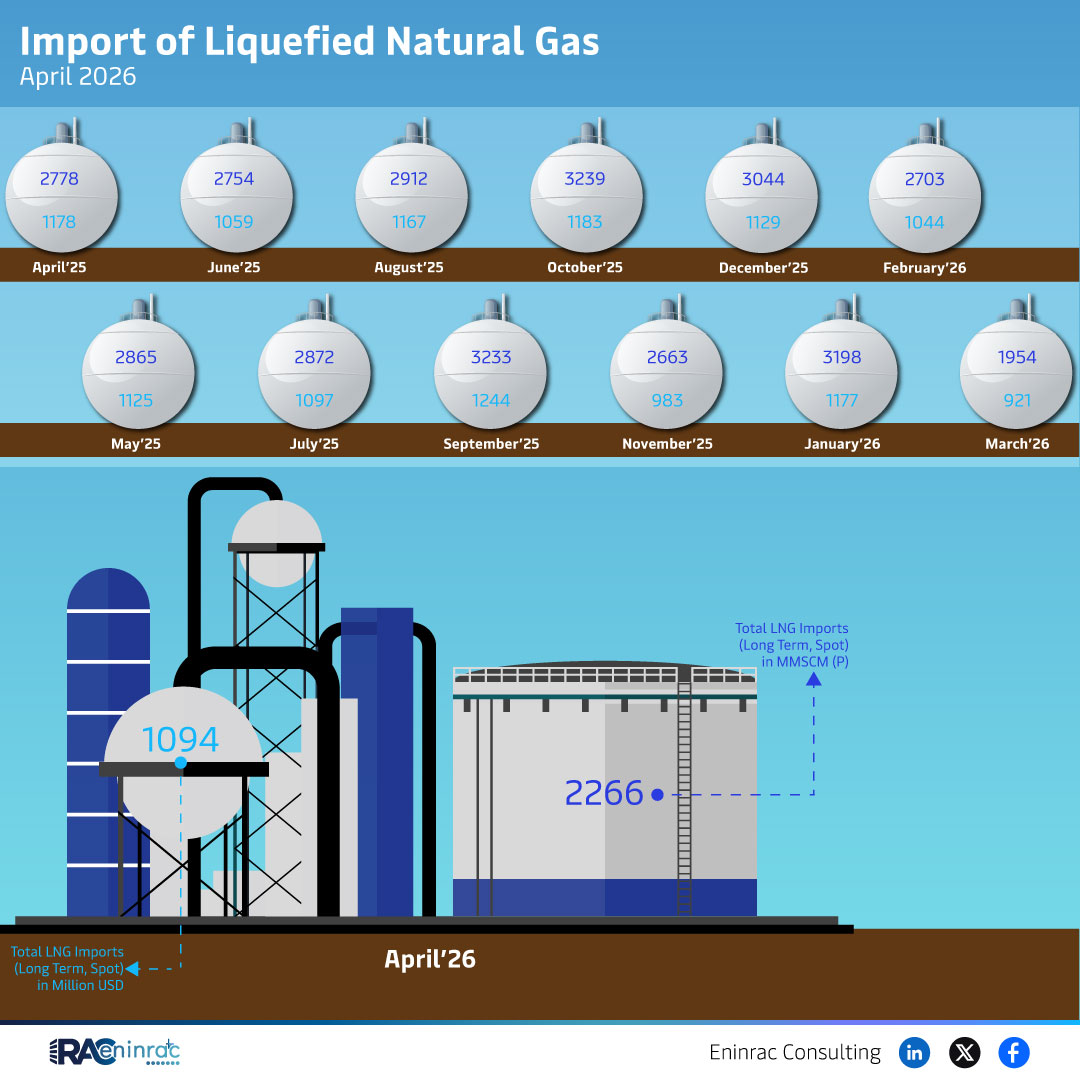

The April 2026 report on liquefied natural gas (LNG) imports presents the total volume of LNG received through both long‑term contracts and spot purchases. Understanding these figures is essential for energy analysts, investors, and policymakers because they reveal market dynamics, supply security, and pricing trends in the conventional energy sector.

What Does the Data Reveal About This Topic?

The data shows the combined LNG imports measured in million standard cubic meters per month (MMSCM). By aggregating long‑term and spot volumes, the report answers the question: how much LNG is actually flowing into the market during April 2026? The answer highlights a steady demand pattern that balances contracted supply with flexible spot market purchases.

Comparative Analysis of Long‑Term vs. Spot LNG Imports

When the two components are compared, long‑term contracts still dominate the import mix, providing a reliable baseline for energy planners. However, spot imports have grown modestly, reflecting tighter global supply conditions and the need for short‑term flexibility. Regions with higher spot activity tend to have more volatile pricing, while those relying heavily on long‑term contracts benefit from price stability. This contrast underscores the strategic importance of maintaining a diversified procurement portfolio.

Impact on Sectors and Industries

LNG import volumes directly affect power generation, heavy industry, and transportation sectors that depend on natural gas for fuel and feedstock. Higher import levels can support electricity generation during peak demand periods, reduce reliance on coal, and help meet emissions reduction targets. For investors, the balance between long‑term and spot purchases signals market confidence and risk exposure. Policymakers use these figures to assess energy security, negotiate future contracts, and plan infrastructure such as regasification terminals.

Key Takeaways

- Total LNG imports in April 2026 are reported in MMSCM, combining long‑term and spot volumes.

- Long‑term contracts remain the primary source of LNG, ensuring supply stability.

- Spot imports are increasing, indicating a shift toward greater market flexibility.

- Regional differences in import composition affect pricing and risk management strategies.

- Higher LNG imports support power generation, industrial processes, and decarbonisation goals.

- Stakeholders should monitor the long‑term vs. spot balance to gauge market sentiment and future price movements.

FAQs

What does MMSCM stand for?

MMSCM means million standard cubic meters per month, a common unit for measuring LNG volumes.

Why are spot LNG purchases important?

Spot purchases provide flexibility to respond to sudden supply gaps, price spikes, or unexpected demand surges.

How do long‑term contracts affect LNG pricing?

Long‑term contracts lock in prices for a set period, reducing exposure to short‑term market volatility.

Which regions typically rely more on spot LNG?

Regions with limited domestic gas infrastructure or those facing seasonal demand spikes often increase spot purchases.

What impact does increased LNG import have on emissions?

When LNG replaces coal in power generation, it can lower CO₂ emissions, supporting climate goals.